Each firm’s governing body is required to review and approve an assessment of whether the firm is delivering good outcomes for its customers, which are consistent with the Consumer Duty. The requirement is for this review to take place at least annually, with firms therefore required to produce and review their first report by 31 July 2024. Firms should, for that reason, be considering the requirements of the assessment and working to tailor their approach to ensure all of these are met.

The FCA has made it clear that these are not attestations for its purposes, but rather are internal governance documents. Nonetheless, and perhaps unsurprisingly, firms can expect FCA to be looking at taking a sample of these reports, and it is likely to form part of supervisory discussions.

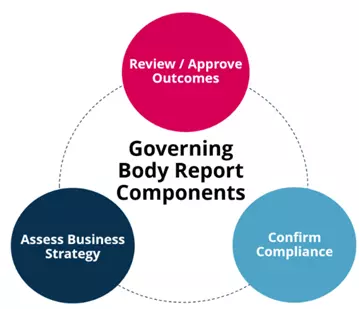

The three components of the Governing Body Report

FCA rules require the following in terms of the Governing Body report, as per PRIN 2A.8. R:

A firm must prepare a report for its governing body setting out the results of its monitoring under PRIN 2A.9 and any actions required as a result of the monitoring. At least annually, the governing body of a firm must:

- review and approve the firm’s report on the outcomes being received by retail customers;

- confirm whether it is satisfied that the firm is complying with its obligations under Principle 12 and PRIN 2A; and

- assess whether the firm’s future business strategy is consistent with its obligations under Principle 12 and PRIN 2A.

When approving the firm’s report under PRIN 2A.8.4R (1), the governing body of the firm must also agree:

- any action required to address any identified risk that retail customers may not receive good outcomes;

- any action required to address any identified instance where retail customers have not received good outcomes; and

- any amendments to the firm’s business strategy to ensure that it remains consistent with meeting the firm’s obligations under Principle 12 and PRIN 2A.

We examine each of the key rule requirements in turn below and how we recommend firms address each aspect.

Reviewing and approving customer outcomes & confirming compliance with the Consumer Duty

Firms will need to provide their governing body with an appropriate amount of information in order to allow them to accurately review the outcomes being received by retail customers.

Remember, it was a part of implementing the Consumer Duty, that firms' ongoing monitoring of outcomes be put in place, and therefore that the necessary data and MI be collected to inform that monitoring. This should be the starting point for the report but if firms are not comfortable that is the case, a good practical first step would be here, and ensuring you know what information you have, should have, and actually need to discuss customer outcomes at the highest level in the firm.

As this is the first report, firms should detail the initial outcomes that their clients were receiving prior to implementing the Duty in July 2023. This should have formed part of the Implementation Plan and assessment, with some explanation of the changes identified to improve those outcomes and comply with the Duty from 31 July 2023. These should then feed into the core aspect of the report; providing the governing body with the evidence and demonstrating the results of the ongoing monitoring that the firm has undertaken in the period to assess the outcomes that its clients are currently receiving.

Taking a critical view of progress is vital: It is important that firms not only detail positive outcomes which their clients are receiving, but also evidence any poor outcomes being received. It is equally important for firms to be open and honest about these challenges, as that then provides the opportunity to demonstrate that they are being captured, and what is going to be done about it. The FCA rarely expects perfection in compliance, and will always look favourably on a firm that is able to acknowledge concerns – of course, with the key being that the firm has a clear plan of action to remediate any issue or shortcomings.

Any identified shortcomings in customer outcomes should be presented with analysis of impact and root cause. The FCA has specified that firms should also consider whether one or more groups of customers is receiving worse outcomes compared to any other group. This means the structure of the report should consider how best to present the MI and reporting data for different customer segments, as well as what the KPI and KRIs were, that now lead to any conclusions. Vulnerable customer activity and considerations in terms of outcomes is a key consideration to de demonstrated in the annual report.

As noted, where risks or poor outcomes are identified, the report should provide a detailed overview of actions undertaken or planned to address these findings. It will be the responsibility of the governing body to agree these actions and they will therefore need sufficient oversight of the issues, ramifications and solutions, to allow for informed discussions to be had, and decisions to be taken.

The report should clearly set out a plan for how any poor outcomes will be rectified, but also provide similar analysis and follow-up actions for any areas which require general improvement. The FCA have repeatedly stated this is not a 'tick box exercise', nor is it 'once and done' and so firms should be looking to constantly develop their approach and so general comments on future looking development of the firm's Consumer Duty strategy should also feature in the Governing Body's commentary.

Assessing business strategy

In the report, firms also need to demonstrate an assessment of their current and forward-looking business strategy and whether it is consistent with acting to deliver good outcomes under the Consumer Duty. As the FCA puts it, how are you ensuring that what you are doing is customer focused?

As part of the process firms should also be considering what market insight they have gained throughout the implementation of the Consumer Duty. For example, this is a great opportunity to review what information has been gathered from within the distribution chain and consider how this aligns with your stated intentions and strategy. Peer data is also useful to include if available and gleaned in the period.

This is also an opportunity to demonstrate that the Consumer Duty has been embedded into the firm's governance and into its culture. While it is a compliance requirement to consider this aspect of the assessment, it is also good practice to show that good customer outcomes are an integral part of any strategic thinking. If that is not already the case, the report should be seen as a vehicle for pushing that consideration into strategic discussions – supported by tactical plans.

Similar to other areas of the report, where the firm finds areas where its strategy is not aligned with the Consumer Duty, required changes and actions should be identified and agreed to ensure that the business strategy is, and will continue to be, working to deliver positive outcomes for consumers. In addition, while it's important to consider strategy alignment - if there is misalignment, then it is equally important to reflect upon the forward-looking approach to ensure alignment of future strategy.

Points to consider in terms of the governing body confirming compliance with its obligations under Principle 12 and PRIN 2A

Governance

A key part of ensuring compliance with the Consumer Duty will revolve around each firm having sufficient governance in place. The firm's governing body is ultimately responsible for signing off compliance, with the annual assessment being the tool to do so. It is therefore essential that the governing body's role is sufficiently defined.

It is important to note that the FCA has emphasised the expectation that, where possible, there should be a distinct differentiation between Executive Committees and decision makers, and the governing body with regard to the Consumer Duty. The executives own the delivery of the Consumer Duty whilst the governing body provide review and challenge, setting the strategy and obtaining assurance from the business that it is delivering outcomes in line with the Duty.

The firm's governing body should therefore be working with their executives to challenge and drive them as appropriate, and the FCA will be looking to see that this is the case – that there is evidence being presented, considered and that push back occurs when needed (with clear remedial actions as appropriate). Governing bodies should also ensure they understand what information they want to receive to allow them to challenge and ultimately approve that outcomes under the Duty are within expected tolerances, and where that is not provided, to again push back. From a practical perspective, that means that those involved in producing the report are understanding now what those requirements are, if not already agreed.

This is an important opportunity to show that governing bodies have been giving the Consumer Duty the right level of attention, and not sitting back thinking the job was completed last summer. Indeed, it can demonstrate that lessons learned from implementation have been actioned.

We expect the Non-Executive Directors (NEDs) of each firm to play a key role in providing independent critical challenge to the information that is being provided. The FCA have recommended firms appoint a NED to be their Consumer Duty Champion for this purpose but regardless of this appointment, they will be essential for scrutinising the work undertaken.

For smaller firms, where independence for assessing delivery can prove a challenge, the FCA has recommended the introduction of an 'independent critical friend'. While it has not expanded on who that might be, this independent critical friend is seen as a person who would bring a level of objectivity and independence when reviewing the annual assessment.

Metrics

A key part of the report will be to provide the relevant data and metrics which have been tracked to demonstrate customer outcomes. A practical point to consider is that the FCA has said that it expects these reports to demonstrate that firms are taking data-led approaches, so this is the time to demonstrate that is the case.

Whilst we are aware that most firms will have already identified the relevant metrics and will be producing ongoing MI, it is important for the preparation of the report that these metrics are subject to critical challenge.

The metrics need to be assessed and challenged to fully understand what they are telling your firm with regard to how well you are complying with the customer outcomes.

Firms should also look at the KPIs and KRIs which are being tracked across the business to consider and assess what information they are providing in relation to customer outcomes, for example firms could consider complaints data, claims ratios, fair value assessment results and customer understanding testing feedback. The data should be supported with explanatory commentary and case studies to help create the full picture of the work undertaken and its outcomes. This will allow the governing body to make effective decisions and challenge where appropriate.

Consideration should also be given to how those metrics are informed by information provided by any other co-manufacturer, or others in the distribution chain. Do the firm's metrics appropriately take these into account – for example, does the fair value assessment reflect any pricing or sales data provided by a dealer or broker further down the chain, which demonstrates what is happening in practice?

Forward Looking Nature

The FCA have been keen to set expectations that the assessment should not only detail the current customer outcomes, but it should also detail plans to improve these outcomes going forward. Similarly, the report should outline how the firm plans to continue to build on the work already undertaken and how this will tie into the business strategy. For example, if your firm also provides unregulated services or products, you may wish to detail how you plan to update these offerings to be more aligned with the Consumer Duty and providing good customer outcomes.

Future assessments should also be building on prior ones to demonstrate these plans coming to fruition and progress being made, ensuring that this is not a 'once and done exercise'.

The Importance of the Consumer Duty Champion

The FCA has clearly defined the role of the Consumer Duty Champion which is to, alongside the Chair and the CEO, ensure that the Consumer Duty is raised and discussed in all relevant discussions and to challenge the governing body to embed the Consumer Duty into its business outlook.

Given this is the case, we highly recommend that firms engage with their Consumer Duty Champion early on and throughout the assessment drafting process to discuss the framework and contents, and to ensure the governing body is comfortable with the report prior to it being finalised and issued.

Timing

The deadline for the report to be reviewed and approved by the governing body is 31 July 2024.

The annual report needs to enable the governing body to assess the firm's compliance with the Consumer Duty. Appropriate time therefore needs to be allocated to collate the relevant information and tailor it for the governing body's purposes. In addition, time needs to be allowed for the governing body members to digest the contents and challenge as necessary.

As a result, firms should ideally already have started this process to ensure they have adequate time to prepare a comprehensive report. Of course, if this is the not case, there should be prompt discussions taking place to agree a plan of action to ensure the process begins as soon as practicable. Identifying, the key owners of workstreams and actions, key stakeholders (both within the firm and not just the governing body itself), and what the key milestones are. This will help ensure that progress can be still be made in good time.

In addition, while the governing body is only required to approve an assessment annually, they are expected to apply the Consumer Duty to almost all governing body discussions and keep track of any specific Consumer Duty issues or challenges. So, hopefully this will also represent a consolidation of discussions over the period since the inception of the Duty and create the impetus for a forward looking governing body agenda where not already in place.

Actions for firms to undertake

We recommend firms firstly make sure they have identified what they require to prepare the assessment, and formulate their internal process for sign-off. This allows each firm to set expectations early about what is required of the various teams, executives and the governing body in terms of information and input. These expectations will ensure the necessary commitment required to meet the end of July deadline.

The second action is to review the commitments you made and intended to deliver on at the start of the Consumer Duty process. Consider how you wished to position yourself against your peers in terms of the services offered and culture, and how your current assessments correlate with this. For example, is the data complementing or contradicting those commitments and what actions are following on from these results?

Finally, we encourage firms to use this process to take a step back and reflect on how the business is now operating with regard to the Consumer Duty. This is the time to really consider the implementation of the Duty from a holistic point of view, challenging the business not only against the customer outcomes, but also Principle 12 and the Cross Cutting rules.

Recent publications reinforcing your approach to the Governing Body Report

Consumer Duty implementation: good practice and areas for improvement

In the above FCA publication of 20 February 2024, (read our summary here), the FCA re-stated that under the Duty, the outcome the FCA wants in terms of culture, guidance and monitoring is the requirement for firms' management and Boards to use data to identify, monitor and confirm they are satisfied that their customers’ outcomes are consistent with the Duty and have taken action when customers suffer poor outcomes.

Good outcomes observed so far include an increased focus on the customer at Board level, with firms’ senior leadership teams giving serious consideration to what the Duty means for them at a practical and cultural level, and development of new data and metrics to better understand their customers. Appropriate governance is considered to be where problems are identified – with firms reminded that they should not wait to intervene to address an issue and firms should not be complacent and assume that they can just repackage existing data. FCA want firms to think seriously about what information they need to really understand their customers’ outcomes and issues they may be facing. These are two key tenets of the Governing Body report.

The FCA Business Plan for 2024/25

In the current year plan, The Consumer duty is interwoven through all of the FCA's planned activity and our summary can be viewed here. However, the key headlines are that the FCA renews its commitments to its objective of 'putting customer's needs first' and states that key activities that will be started in the period include supervisory work to test firms’ implementation of the Consumer Duty and to improve firms’ delivery of good consumer outcomes. This will incorporate complaints-handling and root cause analysis, consumer support journeys, consumer understanding, fair value and closed products and services. Firm's handling of Vulnerability will also be a key area of focus and so we recommend that a 12 month look-back on each subject is an important part of the narrative for the Governing Body report.

DWF offers a range of support services to help you achieve the outcomes required under the Duty. Our services are intended to ensure that firms are getting their Consumer Duty obligations right, for the benefit of the business and its customers. In addition, we can work with you to enable you to go beyond compliance and achieve full alignment with the spirit of the Duty.

We have experience in the preparation of Consumer Duty governing body reports and can provide assistance and assurance at a level to suit your needs. We can also provide an independent assessment of the report and act as the 'independent critical friend' for firms which are smaller in size.

We highly recommend that for the first report in particular, you seek external review and challenge around this submission before it is ratified by the governing body, as this will very much be a key document in setting the tone of your regulatory relationship with the FCA in the future.