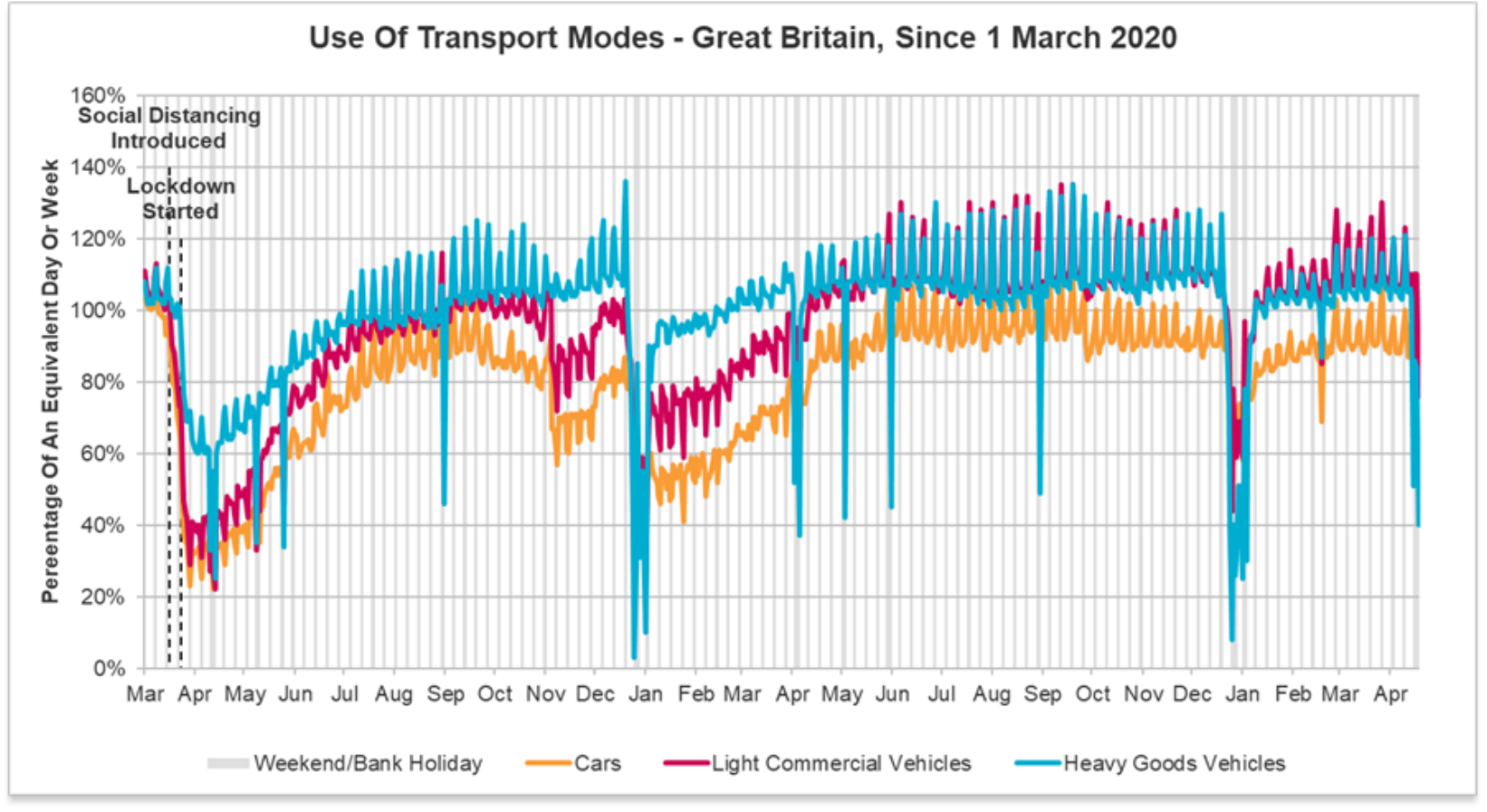

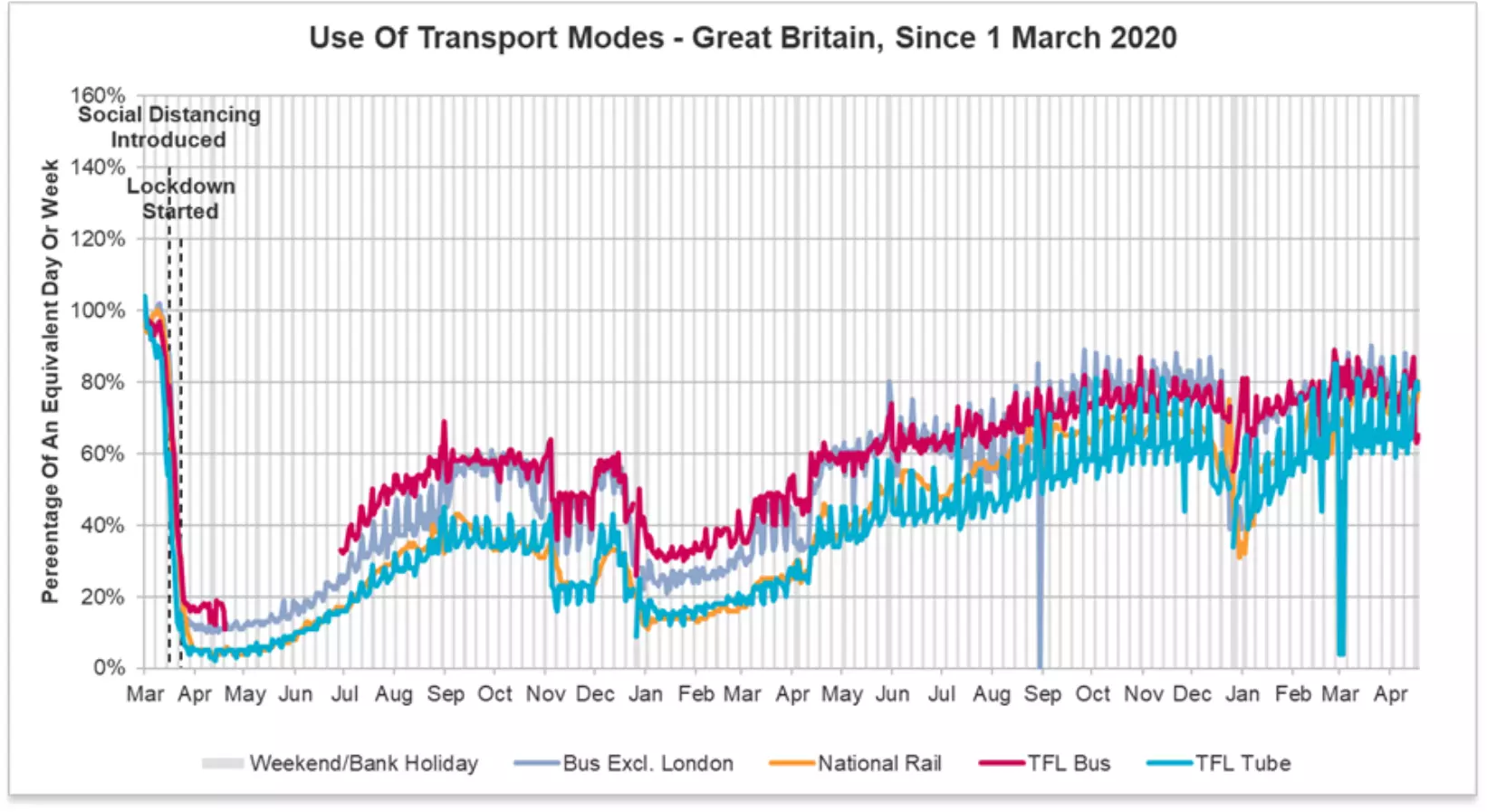

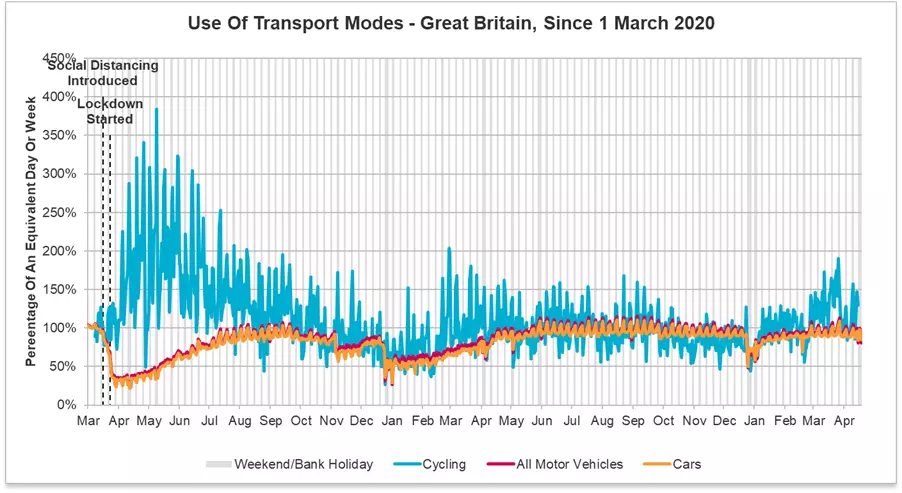

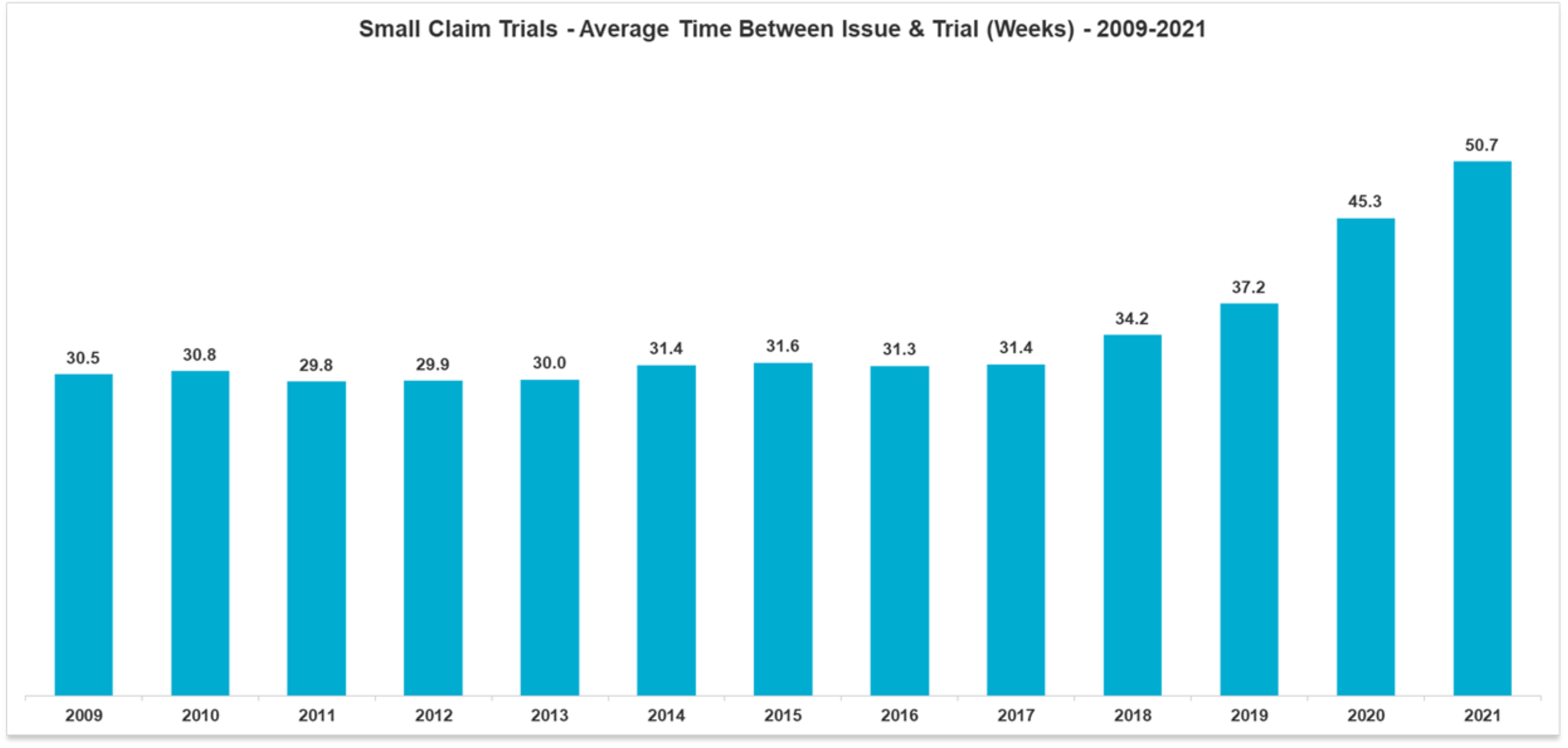

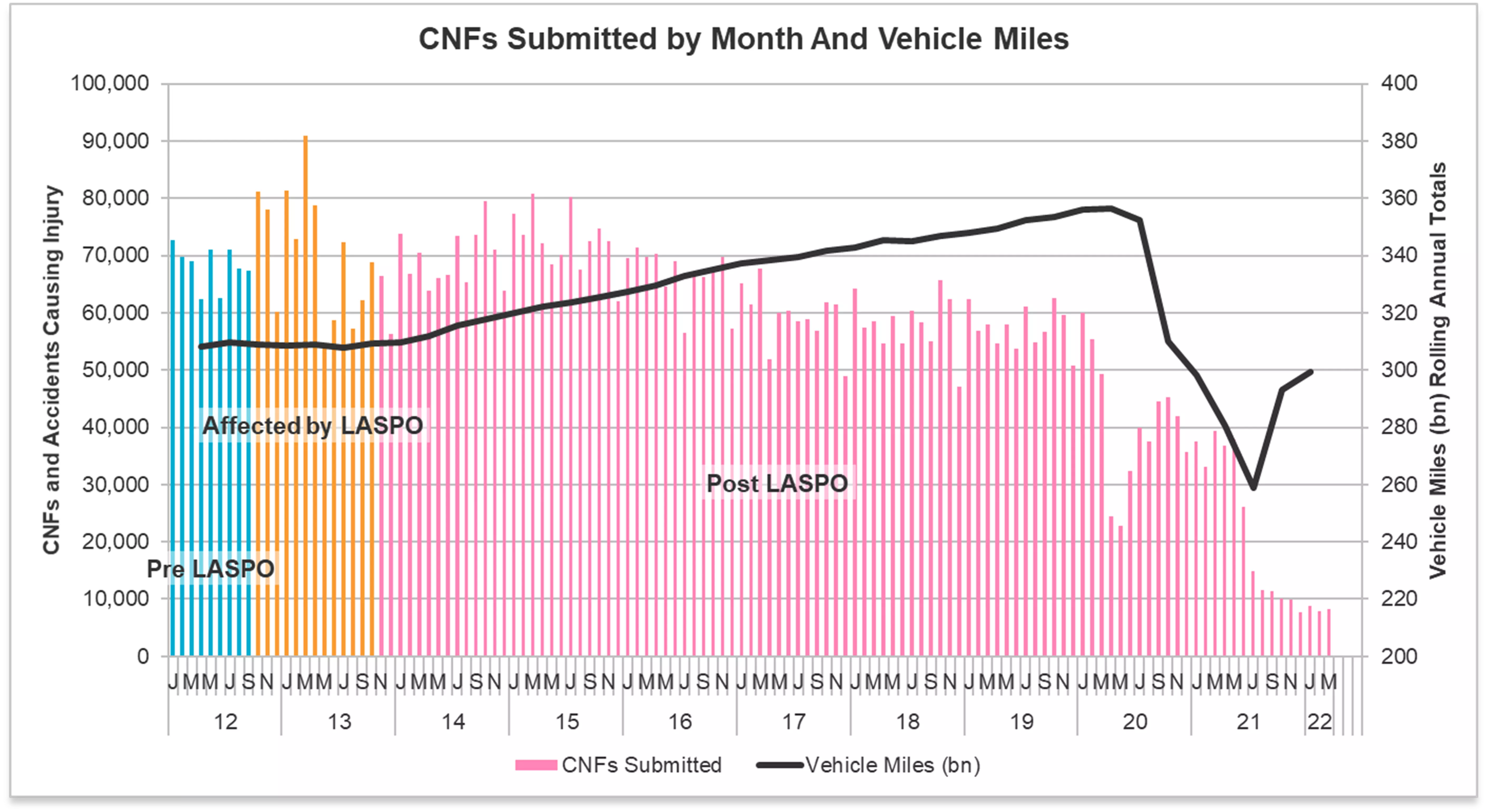

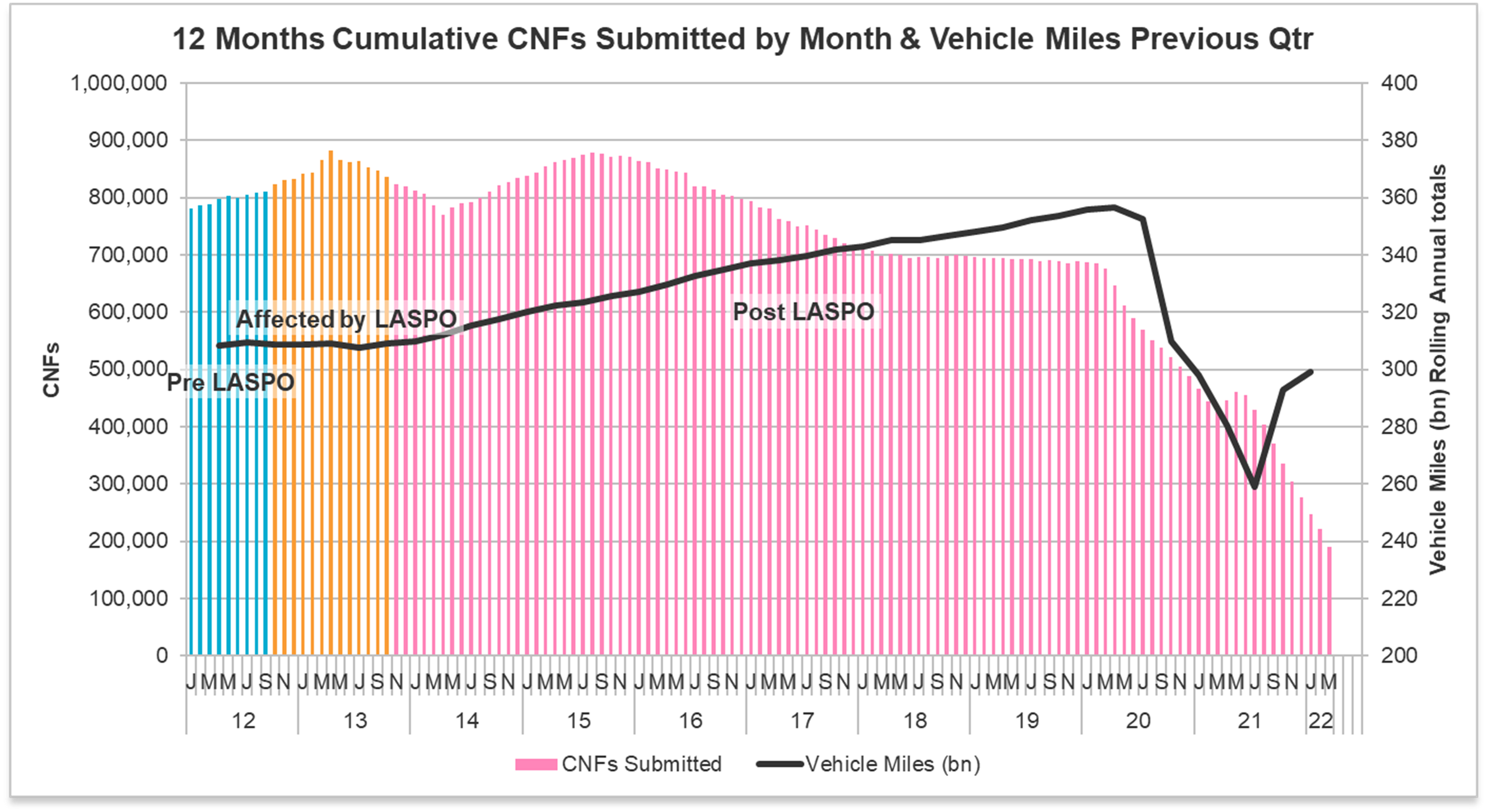

We have a raft of data to review from the OIC, MOJ Portal and MedCo, together with the quarterly civil justice statistics and recent transport data. April traditionally brings CPR updates, and this year is no different, with changes brought in to compel the use of the Damages Claims Portal (DCP) and the long-awaited increase in the SCT limit in EL/PL claims to £1,500.

Choose your location?

-

Global

Global

-

Australia

Australia

-

Canada (FR)

Canada (FR)

-

France

France

-

Germany

Germany

-

Ireland

Ireland

-

Italy

Italy

-

Poland

Poland

-

Qatar

Qatar

-

Spain

Spain

-

UAE

UAE

-

UK

UK

Choose your location?

-

Global

-

Australia

-

Canada (FR)

-

France

-

Germany

-

Ireland

-

Italy

-

Poland

-

Qatar

-

Spain

-

UAE

-

UK